Fraudsters are outpacing traditional verification methods, using AI-generated fake IDs, deepfake facial manipulation, and synthetic identities that can pass weak security checks undetected. Adding insult to injury, a poorly designed ID verification process can drive away legitimate customers as more and more of them simply refuse to go through all the steps if they are seen as tedious.

That is exactly why businesses are widely adopting more modern frameworks for their KYC needs, such as photo ID verification. When organized properly, this method has the potential to make ID checks incredibly fast and secure.

In this article, we’ll break down the problems of outdated identity verification for businesses, introduce a worthy alternative, and explore a couple of customer experience and data privacy considerations along the way.

The costs of a poor ID verification process

Many companies still rely on manual ID checks or outdated document-scanning technology that cannot detect modern forgery techniques. These older verification systems are now getting more and more ineffective against advanced threats such as AI deepfakes, which brings about a range of issues for businesses that employ them.

For instance, in the banking and fintech sectors, synthetic identity fraud has become a major issue. These fake profiles, combining real and fake data, can easily pass through basic ID verification systems, which allows fraudsters to open bank accounts, take out loans, and establish credit histories. And the trends are very concerning: it has been reported that synthetic identity fraud is up 153% from the second half of 2023 to the first half of 2024.

Retailers and e-commerce businesses are also hit hard by stolen and fake identities. A weak ID verification system allows fraudsters to use stolen driver’s licenses and passports to create fake accounts, enabling them to make unauthorized purchases and exploit return policies. MasterCard claims that in 2023 alone, chargeback fraud cost merchants 20 billion USD—a number expected to grow to 28.1 billion USD in 2026.

And it’s not just the immediate financial hit from fraud—it’s the operational, legal, and reputational damage that comes with it. In the famous case of Binance, the cryptocurrency exchange firm was fined an unprecedented sum of 4.3 billion USD in 2023, with founder Changpeng Zhao stepping down from his post as CEO.

Fake IDs are more convincing than ever

Fraud detection is now an arms race. As soon as businesses implement a new layer of protection, fraudsters look for a way around it. Companies that continue to rely on outdated, surface-level ID verification are essentially inviting criminals to exploit them.

A few years ago, the biggest concern was fraudsters altering a real ID—changing a date of birth or swapping a photo. Today, fraudsters are no longer limited by the quality of a forged document. In 2024, AI-powered identity fraud and synthetic identities went mainstream, accounting for 42% of detected fraud attempts worldwide. This means that cybercriminals are more and more often using AI tools to create synthetic IDs that look identical to legitimate ones. And sometimes they don’t just mimic documents—they include believable metadata, embedded security features, and realistic wear and tear.

Subscribe to receive a bi-weekly blog digest from Regula

Photo ID verification as a possible solution

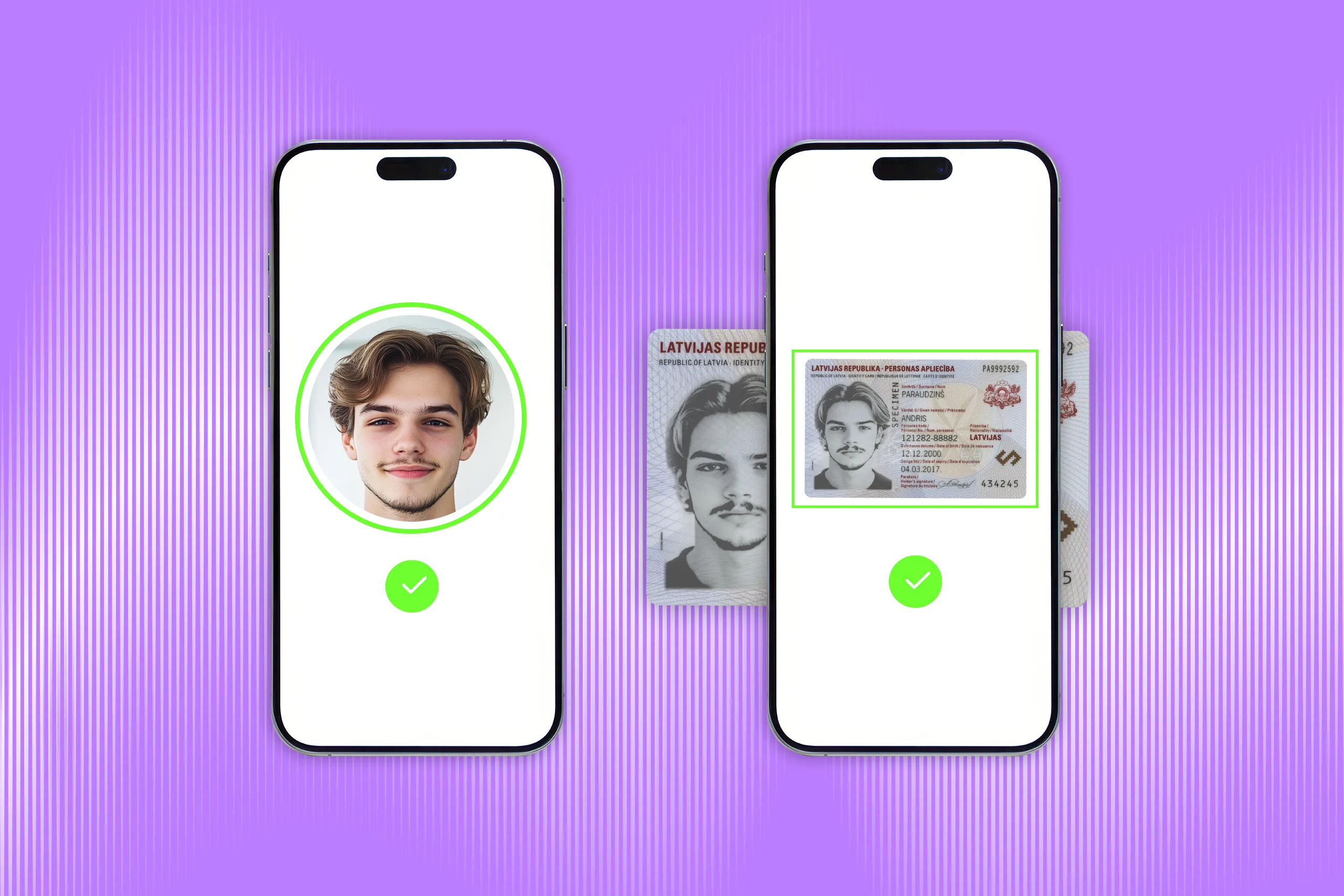

Photo ID verification is a multi-step process that aims to minimize the risks of even the most sophisticated attacks. It confirms a person's identity by analyzing the authenticity of a government-issued ID and matching it to the person's facial biometrics. As opposed to more simplistic forms of business identity verification, this method combines document forensics, liveness detection, and database cross-referencing to prevent fraud.

Accordingly, the process can be broken down into three key steps:

Step 1: Document authentication

The first step is making sure that the ID document itself is real. For that purpose, a real-time identity verification system performs a number of operations, such as:

OCR Data Extraction: Analyzing document layouts and automatically parsing all the personal data fields in IDs (typed, printed, embossed, or engraved) making it instantly ready for further verification.

MRZ (Machine-Readable Zone) check: Reading and validation of MRZs with all the data they contain in accordance with ICAO 9303 and ISO 18013 standards, as well as verification of non-standard MRZ formats.

Barcode and QR code scanning: Processing of 1D and 2D barcodes in ID documents, extracting encoded information and validating the format in accordance with document layout.

NFC chip verification: Reading and verifying embedded NFC chip data from e-documents, ensuring another layer of security by server-side verification.

Document liveness detection: Confirming that the ID being presented is a real, physical document by analyzing dynamic security features and real-time interactions.

Step 2: Biometric matching

Once the document is verified, the next layer of security is facial biometric comparison. Fraudsters now widely use deepfake technology and high-quality masks, so businesses that rely solely on facial recognition are exposing themselves to a major security risk.

That’s why a high-quality biometric system should also include face liveness detection. Similarly to document liveness detention, this feature makes sure that the user is a real person through the analysis of microexpressions, blinking patterns, and 3D facial structure.

There are two types of face liveness detection, depending on the method it uses:

Active liveness detection: Prompts the user to perform randomized actions, such as blinking, moving their head, following a moving object, or even repeating a randomized phrase.

Passive liveness detection: Doesn’t require the user to perform specific movements, thus feels less intrusive. Instead, it prompts users to take a selfie, which drives conversion rates—however, it's slightly less secure.

With the presence of a live person confirmed, the system can then perform 1:1 or 1:N face matching. 1:1 face matching compares a single face against a reference image (typically the ID photo), while 1:N face matching compares a face against a database of many faces.

That said, biometric verification can still produce false positives and negatives, especially if one’s appearance has changed due to aging, facial hair, or medical conditions. That’s why, if possible, there should be manual checks performed by humans after a system flags a suspicious account.

Step 3: Cross-referencing against official databases

Fraudsters can create entirely new synthetic identities using stolen personal data, and your business will otherwise have no way of knowing whether the person actually exists. That’s why even if an ID document appears valid, you still may want to cross-reference identity information with authoritative sources.

Luckily, many identity verification systems help that process by collecting and exporting all biometric data on demand. With this data available, you can check various databases (e.g., government records, PEP databases, credit history reports, and international watchlists) to see:

Whether the person has a history of verified transactions or official records.

If the document data matches information stored in secure national or financial registries.

Whether the person’s identity has been flagged in fraud detection networks or deemed as a high-risk profile.

The customer experience factor

When an ID check is too slow, confusing, or intrusive, customers don’t complain—they simply leave. Banks, fintech platforms, online retailers, and crypto exchanges lose millions in revenue every year because users drop off before completing verification. A customer might be ready to sign up, deposit money, or make a purchase, but if they hit a frustrating ID check, they often choose a competitor instead.

Despite this, many businesses still act as if a bad user experience is an acceptable trade-off for security. That’s a mistake. That’s why instead of making customers take a selfie and multiple photos of an ID, some companies now allow users to verify themselves instantly with facial recognition or fingerprint scanning. And they do so with the help of photo ID verification systems that process documents in seconds while still being extremely secure. Solutions like Regula Document Reader SDK and Regula Face SDK use automated document authentication, biometric cross-referencing, and ML-driven fraud detection to make the process both instantaneous and reliable.

There are also solutions capable of performing Video Ident—an identity verification method where a user undergoes a live or recorded video call with an identity verification specialist or system. In this case, the individual is required to present their ID on camera and perform specific actions (e.g., turning their head or smiling) to confirm they are a live person. This method, although extremely effective, may discourage users as it is more intrusive and time consuming. That’s why it’s important to strike the right balance between security and customer experience. Automated solutions often prove to be the best option.

What earns even more trust from customers is transparency about how their ID data is protected. Companies should provide users with total clarity with their data privacy policies, so that users know where their information is being used and how long it will be stored. That said, customer dissatisfaction is far from the only problem related to data privacy—more on that in the following section.

The privacy concern of photo ID verification

Some businesses collect far more data than they need during the business identity verification process, often without considering the consequences. They demand additional proof of address, full social security numbers, multiple forms of ID, or real-time identity verification via video.

This amount of data may sometimes be necessary, but is also often collected for one of three flawed reasons:

Compliance without clarity: Businesses interpret legal requirements too conservatively, assuming that collecting every possible data point will protect them from liability. In reality, many compliance regulations only require verification of core identity attributes, not full customer dossiers.

Outdated fraud prevention strategies: Some companies still operate on the assumption that more data = stronger security, failing to recognize that fraudsters now use AI-generated synthetic identities that pass even the most rigorous checks. No amount of extra data will stop an advanced identity forgery if the business identity verification system itself is weak.

Data hoarding for future use: Many companies collect more data than necessary simply because they believe it will be useful down the line. But without a clear data retention strategy, this turns businesses into massive security liabilities, storing personal information indefinitely without a plan to secure or responsibly dispose of it.

Why you may be sitting on a privacy time bomb

When companies hold vast amounts of customer identity data, they make themselves prime targets for hackers. In recent years, data breaches involving photo ID verification data have skyrocketed, largely because cybercriminals recognize that identity data is more valuable than credit card information. Once a database containing customer IDs and biometric data is breached, the damage cannot be undone: unlike financial data, which can be reset with a new card number, stolen biometric information is permanent.

One of the biggest threats is credential stuffing attacks, where hackers use stolen identity data from one breach to access other services where the same information is stored. This is especially dangerous for companies that store sensitive customer information in centralized databases without strong encryption or access controls.

That’s why an effective solution is zero-knowledge proof identity verification, a method that allows businesses to confirm a person’s identity without actually storing their personal information. Instead of keeping full identity records, companies can verify users through cryptographic authentication methods that confirm identity details without permanently retaining them.

However, if a business does want to store all the biometric data, the preferred method should be an on-premises or privately hosted IDV solution, as opposed to a cloud-based SaaS. This way, they have full control over the data, and all operations happen within their perimeter, minimizing the risk of leaks. It goes without saying that on-prem solutions are often the only possible option for all sorts of public services, border controls, and even some private banks.

Another option is on-device biometric verification, which allows users to verify themselves using facial recognition or fingerprint scanning on their own smartphones, rather than submitting biometric data to a company’s database. This keeps sensitive data under the user’s control, reducing the risk of mass identity theft in the event of a corporate breach.

The future of photo ID verification: Will we even need cards anymore?

For decades, plastic ID cards and paper-based documents have been the gold standard for verifying identity. However, in recent years we have seen ID verification take a few steps forward with the widespread adoption of ePassports, with over 170 countries issuing biometric passports that store personal data, biometric identifiers, and digital signatures in NFC chips. Similarly, eID cards—digital counterparts to national identity documents— have been deployed in the EU, UAE, India, and various other regions. Unlike traditional ID cards, these electronic documents are much harder to forge, alter, or misuse.

We also are currently witnessing the rise of mobile-based digital IDs such as the EU Digital Identity Wallet. This digital ID for EU citizens, residents, and businesses will allow owners to prove their identity, sign documents, and access government services without needing a physical ID.

Elsewhere, in the U.S., more than ten states have launched mobile driver’s licenses (mDLs), allowing users to store their license directly in their smartphone’s secure element. Apple and Google have both integrated mobile ID support into their operating systems, giving businesses and government agencies the ability to verify identities without requiring a plastic card.

These are exactly the reasons why businesses are also adapting to the new reality, no matter the industry. Companies that still require customers to upload scanned copies of documents may soon find that their ID verification processes are not just slow and frustrating, but completely incompatible with the digital identity systems of the future. In civil aviation, for example, many airports have chosen speed and efficiency, and are already replacing passport control lines with biometric e-gates, where travelers can pass through simply by scanning their face.

As photo ID verification grows in adoption, so does the need for advanced solutions to support it. For instance, ID verification and face biometrics with liveness checks can be carried out by solutions like Regula Document Reader SDK and Regula Face SDK.

These solutions can easily integrate with your existing mobile or web applications. Regula Document Reader SDK processes images of documents and verifies their real presence and authenticity. The software automatically identifies the document type, extracts all the necessary information, and confirms whether the document is genuine.

At the same time, Regula Face SDK conducts instant facial recognition and prevents fraudulent presentation attacks such as the use of static face images, printed photos, video replays, video injections, or masks.